What is ICHRA? A Simple Guide to Individual Coverage HRAs

You may have heard about Individual Coverage Health Reimbursement Arrangements, or ICHRAs, which are quickly becoming a popular alternative to typical group health coverage. Here’s what you need to know.

What is an ICHRA?

An ICHRA is a health benefit model where an employer reimburses employees for their individual health insurance premiums and other qualified medical expenses related to coverage they select. With ICHRA, individuals choose the health plan that meets their personal needs and budget instead of selecting from a predetermined set of group health plan options. While this approach differs from traditional group health insurance, it offers comprehensive coverage for the same essential health benefits.

How does an ICHRA work?

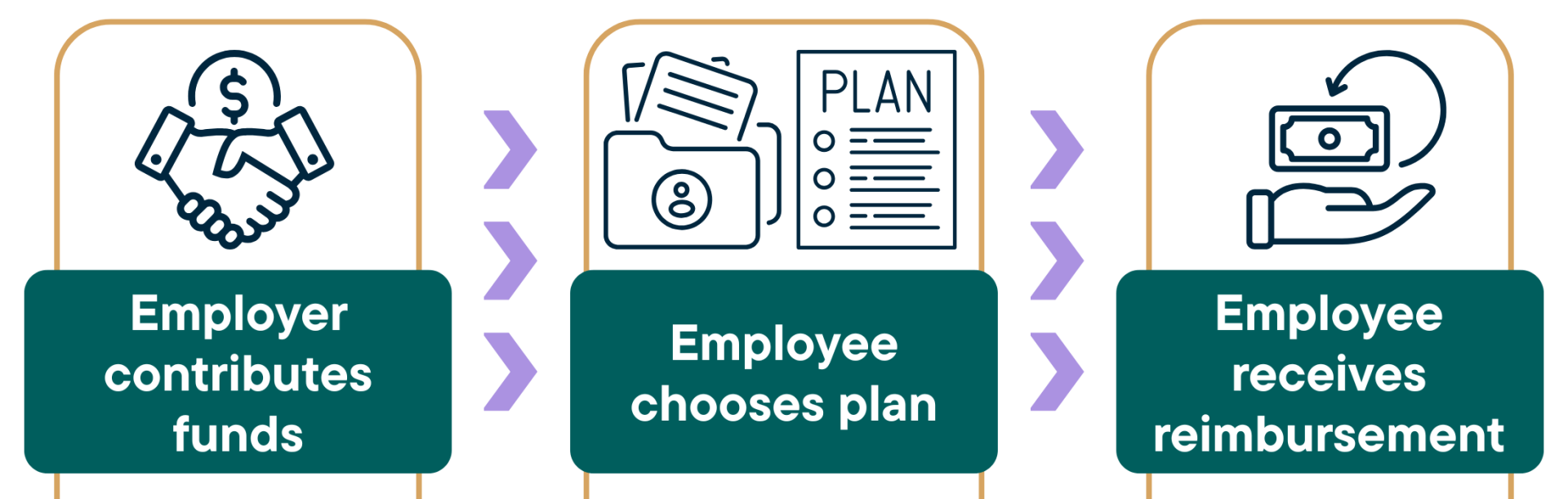

With an ICHRA arrangement, the employer provides a set dollar amount for each employee to utilize toward health insurance premiums and certain medical expenses. Generally, the employer pre-funds the employee’s HRA with the contribution amount. Employees are then able to shop for individual health coverage - a Marketplace plan or a private plan outside the Marketplace - that best fits their situation and desired level of coverage. The ability to shop for their own health coverage means that employees have access to extensive benefits, providers, and health networks. Another perk of the ICHRA model is that employees own their health plan and take it with them if they change jobs, ensuring continuous coverage.

It’s important to know that an ICHRA provides flexibility and autonomy to employees, but also the added responsibility of choosing and enrolling in a plan within the specified Open Enrollment Period (Nov. 1 – Jan. 15) or Special Enrollment Period (varies based on situation). In addition, employees need to be careful to select coverage that includes their preferred doctors and facilities.

Employees are responsible for paying any remaining premium costs beyond the amount allotted by their employer. After an employee selects a health plan, the employer typically deducts the premium balance from the employee’s paycheck on a pre-tax basis.

If this process sounds a bit confusing, know that you’re not alone. The RetireMed team is here to help you navigate ICHRA, whether you’re an employee looking for coverage to fit your needs or an employer looking into ICHRA as a possible health benefit option.

Who can offer an ICHRA and who is eligible?

Any size or type of employer can offer an ICHRA instead of a group health plan to employees. However, employees have certain eligibility requirements they must meet to participate in an ICHRA.

If an employee would like to participate in their employer’s ICHRA program, they (along with eligible household members) must obtain health coverage – either an individual health plan or a Medicare plan (either Medicare Advantage or Medicare Supplement) - that begins at least by the time the ICHRA starts. Employees may opt out of their employer’s ICHRA if they choose.

Employers are not permitted to offer employees the choice between a group health plan and ICHRA. Also, an employee cannot enroll in a group health plan if they have an ICHRA, and they can’t participate in an ICHRA if they’re enrolled in a group health plan.

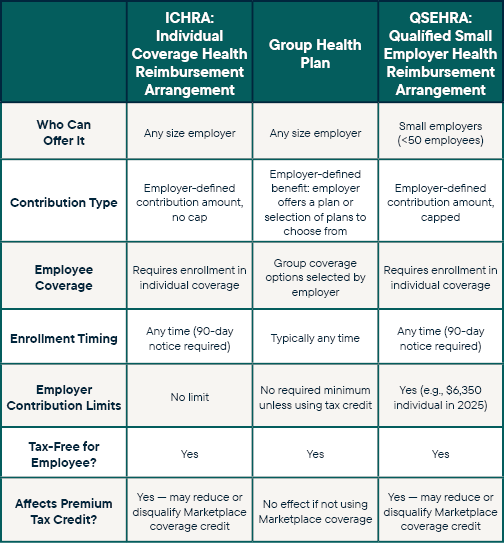

ICHRA vs. Other Health Benefit Options

So, how does an ICHRA compare to other forms of employer health coverage, such as group health insurance and QSEHRA (Qualified Small Employer Health Reimbursement Arrangement)? See our chart.

ICHRA vs. HSA

ICHRA: An Individual Coverage Health Reimbursement Arrangement (ICHRA) is a benefit model where the employer offers employees pre-tax dollars for medical expenses such as premiums, deductibles, and copayments. The funds can be used to purchase a Marketplace (ACA) or Medicare plan (Medicare Advantage or Medicare Supplement).

HSA: An HSA or Health Savings Account is a type of savings account that allows individuals to set aside money on a pre-tax basis for qualified medical expenses. Unlike ICHRAs, funds in an HSA generally cannot be used to pay insurance premiums.

How ICHRA Affects Premium Subsidies

With an ICHRA, individuals purchase individual or Medicare coverage. In the case of individual Marketplace (ACA) coverage, the monthly cost is individualized and based on the estimated income of all household members. Many households qualify for a tax credit, which is a subsidy based on household size and income. This tax credit could reduce your monthly insurance premium for a Marketplace plan. However, if you participate in an ICHRA, you will not qualify for a premium tax credit if your ICHRA is considered “affordable” based on government-mandated standards. Learn more about affordability.

Affordability rules can be complex but are important to be aware of when shopping for an individual health insurance plan, which is why we strongly recommend working with a health insurance advisor who knows the ins and outs of ICHRAs and can help you review ideal options for your needs.

How RetireMed Can Help

Whether you’re an employee trying to figure out how ICHRA works or an employer considering if ICHRA would be a good fit for your company, we’re here to help. Our deep understanding of plan options, regulations, and best practices ensures that you will receive the ICHRA expertise you need. Call our team today!

Share This Article